Exchange Law

- Review of national and district tax declarations.

- Comprehensive advice on tax questions.

- Support in administrative processes related to tax issues.

- Support in applications for balance receivables credit balances and refunds.

- Transfer pricing.

- Tax planning.

- Comprehensive advice on the solution of possible contingencies related to exchange rates.

- Foreign exchange and foreign investment: Handling of all types of currency trading and clearing accounts, assistance in filling out forms and any procedures before foreign exchange market intermediaries and the Central Bank (Banco de la República).

- Advice on import procedures (customs regime and foreign trade) and export regime.

Crypto-asset regulation in colombia: recent trends

The regulation on crypto-assets is a relevant index to determine the digital business climate in a country. Like any emerging technology, its early adoption in a market and adequate regulation can be an important step in the digital transformation processes in companies, the government and support digital entrepreneurship. The efficiency and data decentralization of blockchain and cryptocurrencies generate disruptive effects in certain markets and may also create concern about eventual illegal activities deriving from the technology’s relative anonymity.

In Colombia, several public entities have issued regulation and opinions on crypto-assets. This is precisely the first trend that we want to highlight. In Colombia there is a diversity of public entities that have touched upon different legal issues related to crypto-assets, namely: financial, exchange, tax, commercial, compliance and contractual issues, among others.

The following is a list with the main existing regulation and opinions:

(a) Financial Superintendence, Chapter XVIII External Circular Letter No. 041 of 2015;

(b) Decree 2555 of 2010.

(c) Regulatory Decree 1068 of 2015 (article 2.17.2.4.1.1);

(d) External Resolution No. 8 of May 5, 2000;

(e) External Resolution No. 1 of May 25, 2018;

(f) External Circular Letter No. DODM-144 of September 14, 2018;

(g) External Circular Letter No. DECIP-83 of August 27, 2021;

(h) Central Bank Opinion No. JDS-03409 of February 16, 2011;

(i) Central Bank Opinion No. JDS-19704 of September 12, 2016;

(j) Central Bank Opinion No. C19-110904 of June 21, 2019;

(k) Central Bank Opinion No. C21-70969 Q21-4417 of December 9, 2021;

(l) Financial Superintendence Opinion No. 2020079520-001 of May 15, 2020.

This is an effect of the transversal use of crypto-assets in different economic sectors and for different activities. However, if greater legal certainty is sought, the government could adopt a public policy document defining the vision and direction of the relationship between the public and the private sectors in relation to these digital assets.

In general, the Colombian authorities agree on the following characteristics related to crypto-assets as a basis for their regulation in each legal field and to determine the risks of the crypto title-holders who trade these intangible assets:

- Crypto-assets are not currency, as the only monetary and account unit that constitutes a legal tender and means of payment with unlimited release power, is the Colombian peso issued by the Central Bank of Colombia (bills and coins);

- Crypto-assets are not money for legal purposes;

- Crypto-assets are not a currency, since it has not been recognized as a currency by any international monetary authority nor is it supported by central banks;

- Crypto-assets are not cash or cash equivalent;

- There is no obligation to receive crypto-assets as a means of payment;

- Crypto-assets are not financial assets or investment property in accounting terms;

- Crypto-assets are not securities, so their mention as such or assimilation should be avoided.

The above characteristics have been consistently upheld by different Colombian government documents and denote an interpretation of intangibles that is always based on traditional notions of assets.

Crypto-assets have been defined in Colombia as intangible assets and therefore are likely to be contributed to the capital of corporations, provided that (i) they comply with accounting laws and secondary rules and legal regulations; and (ii) that the partners approve their appraisal. Based on these arguments, the Colombian government expressly affirmed a change in its doctrine, confirming that shareholders can contribute crypto-assets in the form of a contribution in kind. The foregoing, subject to a series of requirements and recommendations, opens the possibility of incorporating crypto-assets as part of the incorporation of companies in Colombia.

Colombian residents who have crypto-assets as part of their assets must declare them in their annual income tax returns. The value for which they must be declared will be for their equity value, either as an intangible asset (investment) or inventory.

On the accounting side, it is recommended that a separate unit of account be created for the recognition, measurement and disclosure of transactions and other events or occurrences that are related to cryptocurrencies, which could well be called “crypto-assets” or “virtual assets”.

If the crypto-assets are traded in a foreign currency, the value of the assets in foreign currency is estimated in national currency at the time of their initial recognition at the official exchange rate, less credits or payments measured at the same official exchange rate of the initial recognition.

Colombian residents who have equipment, resources and work that are integrated into the crypto mining activity, allowing them to obtain virtual currencies in exchange for the services provided in the network and/or by way of commissions, receive taxable income in Colombia, by virtue of the aforementioned criteria. Likewise, it is clear that resident individuals and national companies are taxed not only on their income from a national source but also from a foreign source income and on their assets owned in the country and abroad. From the equity point of view, as long as these coins correspond to intangible assets, capable of being valued, they form part of the equity and can lead to the obtaining of (presumptive) income.

For instance, the purchase and sale of real estate with payment through crypto-assets is an exchange of an asset whose payment will be made through the delivery of an intangible asset. The tax obligations associated with income tax will be those derived from the execution of the exchange contract. Carrying out the exchange will affect the assets of the party delivering the crypto-asset; the payment of the price will generate an equity decrease due to its disposal. On the other hand, depending on the real estate valuation, seller may increase its assets by carrying out the respective exchange, or equate the equity value of the crypto-asset delivered. Consequently, the party delivering the crypto-asset must determine the equity value of said asset, and analyze whether, on the occasion of the exchange, an income for the difference between the tax cost of the asset and the value of its disposal was obtained. The payment of the property through crypto-assets may represent an increase in equity in the head of the property seller if the equity value of the crypto-asset is higher than that of the real estate. The capital increase must be reported in that party’s accounting and income tax return. To the same extent, the real estate seller must determine the equity value of said property, and verify if, on the occasion of the exchange, an income for the difference between the fiscal cost of the real estate and the value of the sale was obtained. The parties must comply with the provisions of the Colombian Tax Statute for the purpose of determining the minimum prices for the sale of the goods subject to the exchange.

As in other jurisdictions, Colombia is no exception for crypto-assets being used in criminal activities. Cases of criminal use, fraud and the use of crypto-assets for payments related to computer attacks and ransomware as well as for payments related to extortion are becoming more frequent. Crypto-assets can also be used as instruments for money laundering, terrorist financing and other criminal activities, in view of which the administrators of the companies that participate in the crypto-asset market must deploy: i) the maximum due diligence in the knowledge of the ends of the operation (including associates, employees, clients, contractors and suppliers, and their final beneficiaries), in regards to the prevention of ML/TF; and, ii) the diligence that a businessman in good faith would take into account to prevent the phenomenon of asset laundering or money from the public being illegally collected or any other damage to the public or private interest being generated through such company. Those who carry out operations with crypto-assets decide in a responsible, conscious and autonomous manner, at their own expense and risk, to assume the possible losses that could be derived from this type of transaction.

The difficulty of clearly defining crypto-assets has been used by criminals to deceive investors and to carry out illegal collection of funds and Ponzi schemes with business models and strategies that can only be carried out by financial entities authorized by the Colombian government.

The growth of the crypto-asset market, in particular cryptocurrencies, depends on the ability of crypto-assets being used in many activities. So, while there is need for a clear regulatory framework that allows measuring risks, it is also important that absolute prohibitions or regulatory disincentives disappear.

In the past two years, a bill that regulates the relationship between wallets, exchanges and platforms in relation to crypto assets has advanced for approval in the Colombian Congress. In the first place, this proposed legislation proposes a series of definitions, among others, the following:

- Wallets: These are the virtual media in which the public and private encryption keys are stored.

- Crypto-assets Exchange Services: these are the following services: (i) Administration of crypto-assets exchange platforms. (ii). Provision of custody and/or storage services for crypto assets. (iii). Exchange or transfer between crypto-assets and fiat currency, or between one or more crypto-assets. (iv). The supplementary or analogous services related to sections i, ii and iii above.

- Crypto Asset Exchange Platform (PIC): These are computer applications or interfaces, internet pages or any other means of electronic or digital communication through which the Crypto-asset Exchange Services are provided.

- Crypto-asset Exchange Service Provider: It is a national business entity or a branch of a foreign company, in charge of operating, managing and guaranteeing the operation of the PIC, registering with the Chamber of Commerce of its main domicile and responsible for compliance with the obligations.

- Unique Registry of Crypto-asset Exchange Platforms (RUPIC): It is an electronic public registry managed by the Chambers of Commerce whose objective is to allow anyone to access the information published in said registry, and to verify that the Service Providers of Crypto-assets Exchange as holders are duly registered.

- PIC Operations Manual: Document that contains the requirements and internal parameters of the PIC for the provision of Crypto-asset Exchange Services.

As a principle of interpretation of the crypto-asset market, it is established in the draft bill that crypto-assets are negotiable directly by their owners. The operation of the different crypto assets, their rules belong to the private sphere of the users, who, based on the principles of free market and free competition, must seek to be informed about the risks inherent in trading with assets of any kind.

The Crypto-asset Exchange Service Providers, Colombian or foreigners, must comply with the following requirements:

- Be incorporated as a commercial company domiciled in Colombia or as a branch of a foreign company, and be duly registered in the Colombian mercantile registry.

- Include as the exclusive corporate purpose the performance of activities classified as Crypto-asset Exchange Services.

- Establish and maintain a computer security program that ensures the availability and functionality of its computer systems, protecting said systems and all information stored in them, from unauthorized access, use and manipulation, the foregoing in accordance with the instructions that for this purpose imparted by the Ministry of Information Technology and Communications.

- Adopt control measures aimed at detecting and preventing money laundering and terrorist financing.

- Register in the Special Register for Crypto-assets Service Providers before the Chamber of Commerce of the entity’s main address, indicating the web domain and the information determined by the Ministry of Information and Communication Technologies.

- Report to the Financial Information and Analysis Unit the information that is required in compliance with money laundering regulations.

- Comply with the Colombian personal data protection regulations.

- Implement KYC and customer Due Diligence measures.

- Have an Operations Manual for the operation of the PICs that it manages, approved by the Ministry of Information Technologies and Communications.

According to the proposed bill, the Crypto-assets Exchange Service Providers are prohibited from:

- Offering or paying consumers interests or any other return or monetary benefit for the balance that they accumulate over time or maintain or for any operation directly or indirectly related to the exchange that they carry out with crypto-assets.

- Transferring under any title, lend or encumber crypto-assets or any other resource owned by consumers, stored by the Crypto-asset Exchange Service Provider, without the express authorization of the consumer.

- Developing any kinds of commercial network or multi-level marketing activity with crypto-assets, as well as their financial intermediation. Likewise, the administrators or service providers of crypto-asset exchange platforms may not allow the commercial distribution of crypto-assets to be carried out on their platforms through network or multi-level marketing activities or similar.

- Refraining from carrying out any conduct that leads to the massive and regular collection of funds from the public that additionally implies the absence of consideration in present or future goods or services that justify it or, even if such consideration exists, does not have a reasonable financial explanation.

The model proposed in this draft bill does not comprehensively regulate the different legal aspects of crypto assets. The relationship between some of the agents in the ecosystem can set aside a holistic vision that is necessary to obtain the benefits of intelligent regulation. It is not clear if the Financial Regulation Unit of the Colombian government agrees with the content of this bill.

To sum up, in Colombia there is a regulatory trend that has been transforming from a prohibition on the use of crypto-assets towards a vision more associated with the risks inherent in the market for these digital assets. The regulation remains disperse since different Colombian public entities with market supervision and surveillance functions have issued rules and opinions related to accounting, tax, contractual, exchange and financial issues, among others. An effective coordination between the different public entities that regulate crypto-assets is necessary to achieve legal certainty and stimulate the use of these digital assets as well as to generate a business environment that allows attracting investment. It is necessary to wait and see if the draft bill that is in progress becomes law so that wallets, exchanges and crypto-asset offering platforms in particular, are regulated more specifically in terms of their registration and duties as well as their liability towards consumers and users of crypto-assets.

The Council of State clarifies the requirements for the application of the VAT exemption for services rendered in the country and used exclusively abroad

In order for exporters of services to benefit from the VAT exemption, they must comply with a number of requirements (section c of article 481 of the Tax Statute) among which are that the services are rendered from Colombia; that their use or exploitation is carried out exclusively abroad; and that the beneficiary does not have any business or activities in Colombia.

In its ruling number 27317 of July 19, 2023, the Council of State has reiterated that a service is understood to be used abroad when the benefit or profit derived therefrom takes place outside the national territory, provided that the activities that constitute the service, whose export is claimed, have been performed in Colombia, the foregoing in accordance with the provisions of paragraph c) of Article 481 of the Tax Statute.

Thus, the requirements for the VAT exemption on the exportation of services are as follows:

- That the service had been rendered in Colombia to a foreign country.

- That the service was used or consumed exclusively abroad.

- That the consumer is one or several persons, individual or business entity, without any business or activities in Colombia.

- That, even if the consumer is national or has ties with Colombia, the service object of the exemption must be used abroad.

- That the other requirements indicated by article 2 of Decree 2223 of 2013 were met which are:

- To be registered as an exporter of services in the RUT.

- Keep the invoices, service offers and/or quotations with their respective acceptances, the contract between the parties or the purchase/service order plus the acknowledgement of receipt of the service.

- To have the certification of the provider or legal representative stating that the service was provided to be consumed exclusively abroad.

The Council of State explained that a difference exists between the acquisition of a service in Colombia and its use abroad. Even if a service is acquired in national territory, if this (i) is provided from Colombia (ii) is consumed exclusively from abroad as, for example, a medical assistance service that is acquired in Colombia to be used outside the territory in case of a contingency (iii) that the service is used abroad by a person without business or activities in Colombia for the specific service as in the case of the traveler and (iv) even if he/she has them, this service is used exclusively abroad because the advantage, benefit or consumption of the same is given outside Colombia.

It is always necessary to identify the final destination of the operation where the service acquired from Colombia is going to be materialized in order to apply section (c) of article 481 of the Tax Statute. The concept of business or activity cannot be confused as all the actions that are performed in Colombia to acquire the service that will be performed abroad, since the previous acts do not prevent the application of the exemption since, in the end, the client must benefit from the service abroad. Nor can the non-exemption be claimed if the consumer of the service abroad has businesses unrelated to the business subject to exemption in Colombia if the activity to be exempted complies with all the requirements of art 481 already referred to.

Obligation to enter data in the Beneficial Ownership Single Registry “RUB”

By: Juan Simon Larrea & Javier Moya

With the issuance of Law 2155 of September 14, 2021 “Social Investment Law”, articles 631-5 and 631-6 of the Tax Statute (hereinafter “ET”) were modified and the Single Registry of Final Beneficiaries (hereinafter “RUB”) was created, which was regulated by Resolution 164 of December 2021, subsequently modified by Resolution 37 of March 17, 2022, issued by the National Tax and Customs Directorate “DIAN”. In addition, the Identification System for Structures Without Legal Personality “SIESPJ” was created.

Acronyms and Abbreviations

- SWLP – Structure Without Legal Personality

- RUB – Single Registry of Beneficiary Owners

- RUT – Single Tax Register

- SIESPJ – Identification System for Structures Without Legal Personality

- BO – Beneficiary Owner / Final Beneficiary

- DIAN – Directorate of National Taxes and Customs

1. Single Register of Beneficial Owners “RUB”

1.1. What is RUB?

The RUB is the registry that is an integral part of the Single Tax Registry (RUT) that must be completed virtually and in which legal entities and unincorporated or similar structures must provide the information of their Beneficiary Owners.

1.2. Who are the Beneficiary Owners of legal persons?

The BO of Colombian legal entities, according to article 631-5 of the ET, is any individual who:

- Acting individually or jointly, holds, directly or indirectly (through third parties), five percent (5%), or more of the capital or voting rights of the legal person, and/or benefits in five percent (5%), or more of the assets, yields or profits of the legal person.

In order to better understand the above condition, by way of example we can establish that any individual who is a shareholder of any type of corporation with a percentage greater than 5% is a Final Beneficiary. Likewise, if he/she is a shareholder in this proportion, but indirectly (through a legal entity), he/she would also be considered as a Final Beneficiary.

- Acting individually or jointly exercises direct and/or indirect controls[1] over the legal entity by any means other than those set forth in the preceding point.

Regarding this second condition, the Inter-American Development Bank’s Manual on Beneficial Ownership establishes that the individual may exercise direct or indirect control through a significant percentage of the voting rights, or the ability to appoint or remove members of the board of directors of an entity.

It can also be exercised in other ways. For example, through a power of influence or veto over the decisions made by an entity, through agreements between shareholders or partners through family or other ties with decision makers, or through the ownership of negotiable obligations or other debt securities of an entity convertible into shares.

Thus, according to the manual and the recommendations issued by the Financial Action Task Force (FATF), the beneficial owner must be identified through other means such as exercising control without having an ownership interest in a company.

Now, as a residual condition and only when no beneficial owner is identified (in non-corporate legal persons such as: national or foreign non-profit entities) under the criteria indicated above, the individual who holds the position of legal representative shall be considered as the beneficial owner, unless there is an individual who holds greater authority in relation to the management or direction functions of the legal person, in which case the latter individual must be reported.

1.2.1. Who are the BO in unincorporated or similar structures?

The Beneficiary Owner of an Unincorporated Structure o structures without legal personality (hereinafter referred to as “ESPJ”) are the individuals who hold the status of:

- Trustor(s), settlor(s), constituent(s) or similar or equivalent position.

- Trustee(s) or similar or equivalent position.

- Trustee committee, finance committee or similar or equivalent position.

- Trustee(s), beneficiary(ies), or conditional beneficiary(ies); and

- Any other individual exercising effective and/or final control or having the right to enjoy and/or dispose of the assets, benefits, results or profits.

Based on the above, a resident or non-resident individual who holds five percent (5%) or more of the capital of a legal entity and/or benefits from five percent (5%) or more of its assets, yields or profits, carries out transactions with the assets of another person or makes decisions in the administration, direction or management of a company or benefits from the activities of a private non-profit entity, is a beneficial owner and must be registered in the RUB. Likewise, if he/she holds the status of beneficiary in the ESPJ.

1.2.2. Who is obliged to provide information?

The following legal entities and structures without legal personality or similar, are required to provide information in the RUB, with respect to their beneficial owner:

- Corporations and national profit or non-profit entities in accordance with the provisions of Article 12-1 of the ET, including those whose shares are registered or listed in one or more stock exchanges.

- Permanent establishments, i.e., those that have a fixed place of business in the country, through which a foreign company, whether a corporation or any other foreign entity, or individual without residence in Colombia, performs all or part of its activity.

- National companies and entities, including those listed on the stock exchange and registered in its respective list, that have their main domicile in Colombian territory; or that make effective commercial, administrative or management decisions in Colombia; or that have been incorporated in Colombia.

- All structures without legal personality or similar that were created or that are administered in Colombia or that are governed by Colombian regulations or whose trustee or similar is a national legal person or individual resident for tax purposes. An example of the above are trusts or trusteeships, if these are administered or were created in Colombia, their beneficial owner must be in the RUB.

- Foreign legal entities, when the totality of their investment in Colombia is not made in legal entities, permanent establishments and/or ESPJ obliged to provide information in the RUB.

1.2.3. Who is not obliged to provide information?

Public entities, establishments or agencies or national entities or corporations in which one hundred percent of their capital is public are not required to provide information in the RUB. Neither are embassies, diplomatic missions, consular offices or international organizations and agencies accredited by the National Government. Nor are foreign legal entities or structures without legal personality that do not operate in Colombia or are not incorporated in the territory, and even less foreign legal entities whose assets value in Colombia represents less than 50% of their total assets. In addition, any other situation that does not meet the requirements described in the preceding paragraphs.

1.2.4. What information must be provided and what is the procedure to register data for legal entities in the RUB part of the RUT?

The RUB is an integral part of the Single Tax Registry (RUT) before the DIAN, for legal entities, and the information that must be submitted is the following, according to article 8 of resolution 164 of 2021 DIAN:

- Type of document

- Identification number and country of issuance

- NIT or functional equivalent and country of issuance.

- Names and Surnames

- Date and country of birth

- Country of Nationality

- Location: Country of residence, department or state, city, zip code, e-mail address

- Criteria for determining the final beneficiary

- Percentage of participation in the capital of the legal entity.

- Percentage of benefit in the yields, results or profits of the legal entity, structure without legal entity or similar.

- Date from which it has been the beneficial owner or the condition exists.

- Date from which it ceases to have the quality of beneficial owner or the condition no longer exists.

1.2.5. Deadline for registration of information by legal entities in the RUB

According to the same Resolution 164 of 2021 of the DIAN, modified by Resolution 37 of 2022 and Resolution 1240 of 202, the information must be provided no later than July 31, 2023, by legal entities, structures without legal personality or similar structures constituted or created prior to September 30, 2022.

In the case of legal entities, unincorporated structures or similar that are constituted after September 30, 2022, they will have 2 months from the registration in the Single Tax Registry RUT or in the Identification System of Unincorporated Structures SIESPJ.

1.2.6. What is the due diligence principle?

This principle is developed in Article 12 of Law 2195 of 2022 through which measures of transparency, prevention and fight against corruption are adopted and provides that anyone who has the obligation to deliver information to the RUB, must carry out due diligence measures that allow identifying the final beneficiary(ies) taken these criteria:

- Identify the individual, legal entity, ESPJ or similar that enters into legal business or state contract.

- Identify the beneficial owner(s) and the ownership and control structure of the legal person, legal entity, JSE or similar and verify the information.

- Request and obtain information on the purpose of the legal business or state contract when the state entity is the contracting parties and in order to obtain information on the corporate purpose of the contractor.

- Perform ongoing due diligence on the business or contract by examining that the transactions are consistent, its business activity, risk profile and source of funds.

1.2.7. Which authorities have access to the RUB?

According to Article 13 of Law 2195 of 2022, the Comptroller General of the Republic, the DIAN, the Prosecutor´s General’s Office, the Superintendence of Industry and Commerce, the Superintendence of Finance, Attorney General’s Office and the Financial Information and Analysis Unit UIAF will have access to the RUB.

1.2.8. Penalty

We also remind you that failure to register the data on time may result in the penalties contemplated in Article 658-3 of the Tax Statute, ranging from fines to the temporary closure of the establishment, office, business or headquarters of the owner.

1.2.9 How do I register my beneficial owner in the RUB?

The following link refers to the infographic that explains how individuals and ESPJs, with prior registration in the Unincorporated Structures Identification System as developed below, can register their BO in the RUB.

https://www.dian.gov.co/impuestos/RUB/Documents/Paso-a-paso-2687-RUB.pdf

2. IDENTIFICATION SISTEM OF STRUCTURES WITHOUT LEGAL PERSONALITY “SIESPJ”

The SIESPJ is the identification mechanism, for tax purposes, of unincorporated structures that are not required to register in the RUT. The operation and administration of the System will be the responsibility of the Special Administrative Unit of the DIAN.

2.1.1. What information must be provided and what is the procedure for the registration of data for unincorporated structures in the RUB by SIESPJ

The RUB is an integral part of the Unincorporated Structures Identification System (SIESPJ), for unincorporated structures, before the DIAN and the information to be submitted is the following, according to article 15 of resolution 164 of 2021 DIAN:

1. Type of structure without legal personality or similar.

2. Name and alphanumeric code assigned internally for the identification of the unincorporated or similar structure.

3. Date of creation of the unincorporated or similar structure.

4. Date of termination of the unincorporated or similar structure.

5. Identification number of unincorporated structures – NIESPJ assigned by the Special Administrative Unit of the National Tax and Customs Directorate – DIAN.

6. Start date of administration of the unincorporated or similar structure.

7. End date of administration of the unincorporated or similar structure.

8. Change of administrator of the unincorporated or similar structure.

These percentages are individual and the information must be provided through the electronic system of the Single Registry of Beneficial Owners. Learn the step by step in the following link:

Paso-a-paso-2706-RUB.pdf (dian.gov.co)

In order to register Structures without legal status in the RUB, they must first be registered in the SIESPJ and with the identification provided by the SIESPJ, proceed to register in the RUB.

2.1.2 Deadline to register the information of an unincorporated or similar structure

For unincorporated or similar structures, updates can be made within the month following the event that generated the update.

[1]What is meant by “exercise control”?

To understand what is meant by control, we refer to different sources, among them, the Code of Commerce Arts. 260-261, the Tax Statute Art. 260-1 and Resolution 164 of 2021. It is understood that there is control when a person or a group of persons, natural or legal, exercises dominant influence in the decisions of the administrative bodies. For example, when the shareholders’ meeting makes decisions for the management to implement and the whole company or foundation to undertake new paths. In addition to the influence, these persons must have the right to cast votes constituting the minimum majority of votes in the shareholders’ meeting or in the assembly; or the number of votes necessary to elect the majority of the members of this board of directors. In these cases we may be talking about direct control.

Individuals exercising indirect control, i.e., through an intermediary person or company, are also obliged to be included in the RUB. For example, the owner or sole shareholder of a company that is the parent company of a subsidiary in Colombia that meets the requirements mentioned in previous sections. In this case, it should be registered in the RUB.

As a complement, a situation of control is also present when any of the following situations arise:

- that more than 50% of the capital of a company, directly or through or with the assistance of several of its subordinates or at the same time those that these may have.

- When the parent company and subordinates have in common or separately the right to issue votes.

- When the parent company exercises a dominant influence in the decisions of the administrative bodies of the subordinate company.

One or several legal entities may also be understood as a Parent Company and these parameters apply to them to determine whether they exercise control or not.

“From the above rules it is possible to infer when control is consolidated with respect to commercial companies in Colombia, and the form in which it can be exercised; that is, directly and indirectly; individually or jointly; by participation or simply by dominant influence.” (Concept 220 081921, 2015, S.I.C)

In conclusion, control exists when the decision-making power of a controlled company is subject to the will of another or other persons that will be its parent or controlling company. For example, if a company X in Colombia is controlled by a parent company abroad, and this meets the requirements described in previous paragraphs, the individual who is the ultimate beneficial owner of the parent company must be sought and this person must be registered in the RUB by the controlled company.

The Constitutional Court of Colombia has declared constitutional the Agreement between the Government of the Republic of Colombia and the Government of the French Republic to avoid double taxation

The Constitutional Court (C-443-21 Corte Constitucional) of Colombia has declared constitutional the Agreement between the Government of the Republic of Colombia and the Government of the French Republic to avoid double taxation and prevent tax evasion and avoidance with respect to taxes on income and on assets and their protocol, signed in Bogotá on June 25, 2015. The Agreement is expected to enter into force in a few weeks.

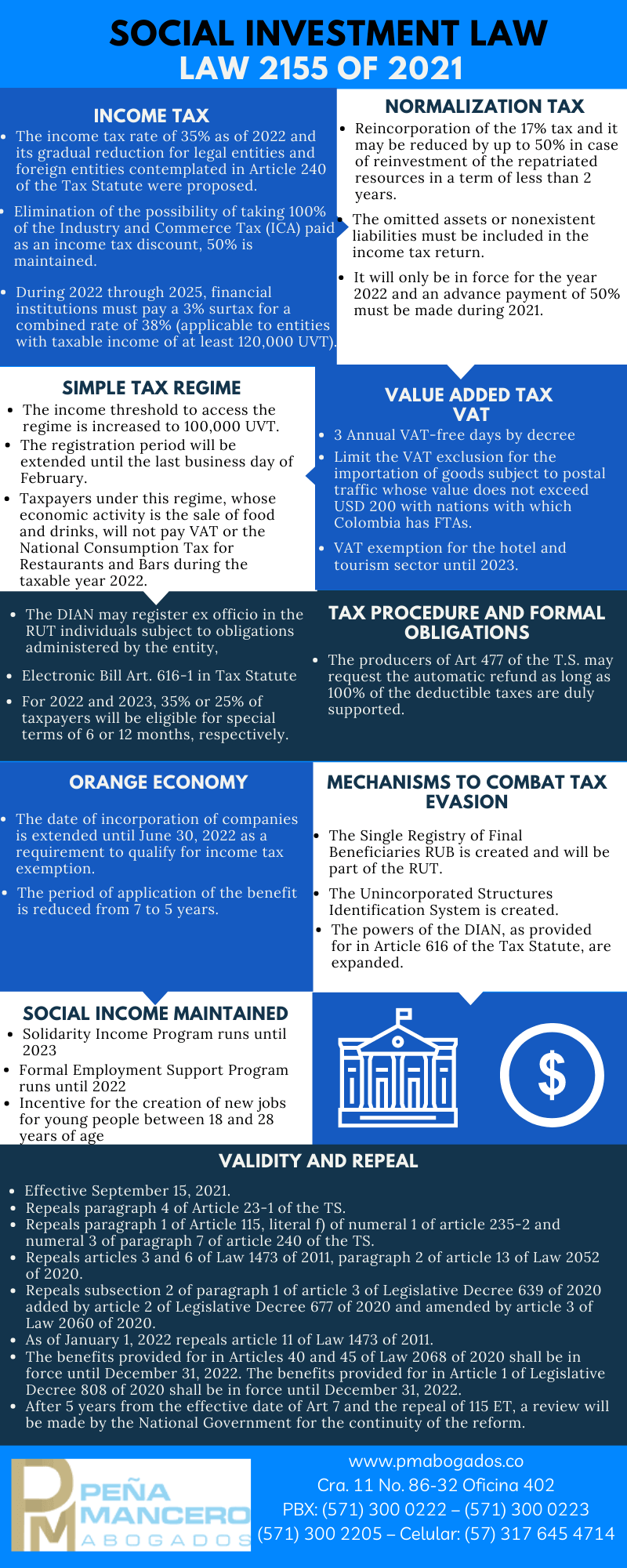

Social investment law, law 2155 of 2021

New regulation on electronic payroll In Colombia

By: María del Pilar Duplat M. – Peña Mancero Abogados

The Colombian tax authority (DIAN by its Spanish acronym) issued resolution 13 of February 11, 2021 regulating the implementation of the electronic payroll system (the “Electronic Payroll Resolution” or the “Resolution”).

Who must submit the electronic payroll to DIAN?

Income taxpayers that are employers or that make payments due to legal or regulatory relationships or that make pension payments, and require to support said costs and deductions in their tax returns.

On a monthly basis, the aforementioned subjects must submit to DIAN a payroll supporting document for its approval or correction.

What is the payroll supporting document?

The electronic payroll supporting document is the document that shows all labor-related payments made by the employer. This document must contain the following information for its creation, transmission and approval by DIAN:

- Expressly indicate that it is an electronic payroll supporting document.

- Employer complete name of the individual or entity, ID Number or tax id number.

- Complete name(s) and ID of the person who receives the payment.

- The Unique Code Number of the Supporting Document of the electronic Payroll (CUNE by its initials in Spanish).

- Internal consecutive number granted by the subject obliged to submit the electronic payroll.

- Contents and amounts of the accrued value of payroll pursuant to the Technical Appendix to the Electronic Payroll Resolution.

- Contents and amounts of the deducted sums from the payroll pursuant to the Technical Appendix to the Electronic Payroll Resolution.

- Total amount resulting from the difference between the total accrued payroll payments minus the total deducted sums from the payroll payments.

- The contents of the Technical Appendix as provided in article 20 of the Electronic Payroll Resolution, regarding the information and contents contained herein.

- The form of payment of the payroll per the Technical Appendix to the Payroll Resolution.

- Date and time of creation of the document.

- Digital signature of the Subject who pays the Payroll in accordance with the DIAN’s requirements of authenticity and integrity of the signature.

- Complete name and ID or tax id number of the software supplier and identification of the software.

When do I have to submit the electronic payroll to DIAN?

The electronic payroll supporting document must be issued and sent to DIAN on a monthly basis, ten (10) days after its creation or issuance.

As of when must the electronic payroll be implemented?

- Implementation Calendar for subjects per the number of employees

| Group | Beginning date of the enabling of the electronic payroll data processing system | Maximum date to start the issuance and transmission of the electronic payroll payment support document and the electronic payroll payment support document adjustment notes. | Range in relation to the number of employees

|

|

| From | Until | |||

| 1 | May 31st, 2021 | July 01, 2021 | More than 251 | |

| 2 | August 01, 2021 | 101 | 250 | |

| 3 | September 01, 2021 | 11 | 100 | |

| 4 | October 01, 2021 | 4 | 10 | |

| 5 | November 01, 2021 | 2 | 3 | |

| 6 | December 01, 2021 | 1 | ||

- Permanent Implementation Calendar

The obliged subjects will have a term of two (2) months from the date in which they make the payroll payments to carry out the enabling of the service and proceeding to transmit the supporting documents of the electronic payroll and its adjustment notes.

The remaining subjects must issue the supporting payroll document and their adjustment notes to request the costs and deductions of the income tax and the VAT deductible taxes, when applicable.

- Implementation calendar for subjects not obliged to issue electronic sales invoices

Subjects not obliged to issue electronic sales invoices must start the enabling of the electronic data payroll service on March 31, 2022; and they must issue and send the supporting document of the payment of the electronic payroll and their adjustment notes, no later than May 31, 2022.

How do I issue the electronic payroll documents?

The enabling procedure is the one that is developed within the electronic invoicing system which must have the function to issue the electronic payroll supporting document pursuant to DIAN’s requirements.

The enabling procedure must be carried out before the date when the subjects must start with the implementation and the term when they must submit the monthly electronic payroll.

If you have further inquiries regarding this new regulation, please do not hesitate to contact us at: info@pmabogados.co

Getting the Deal Through – Tax and Inbound Investment 2007

- Título:Tax and Inbound Investment 2007

- Fecha de publicación: 2007

- Descripción de la publicación: Expert local insight into the regulation of taxation on inbound investments in unfamiliar jurisdictions, covering areas such as: Acquisitions – execution of acquisition, tax treatment of acquisitions, interest relief and deductibility, company mergers and share exchanges and net operating losses; Post-acquisition planning – post-acquisition restructuring, tax neutral spin-offs, interest and dividend payments, extraction of profits; Disposals – types of disposal, gains on disposal and avoiding or deferring the tax on a disposal gain. Including a chapter of Colombia.

- Editorial: Getting the Deal Through

- Autor: Gabriela Mancero

Trademark Infringement in the Digital Ecosystem

Data Protection & Privacy