Newsletter Jun 2026

Decree 0545 of 2026, Issued May 29, 2026

“Whereby guidelines for the environmental planning of the Bogotá Savanna are established”

The National Government issued Decree 0545 of 2026 for the purpose of establishing guidelines for the environmental planning of the Bogotá Savanna, pursuant to the mandate set forth in Article 61 of Law 99 of 1993, which recognizes this region as an area of national ecological interest.

These guidelines constitute binding environmental planning criteria and rules of superior legal hierarchy that must be incorporated by territorial entities and considered by environmental authorities in the exercise of their respective powers.

The Decree applies to Bogotá D.C., the municipalities that comprise the Bogotá Savanna, and the authorities and entities responsible for territorial planning and land-use management.

The Bogotá Savanna encompasses 31 municipalities. The Decree applies in its entirety to: Cajicá, Chía, Cota, Funza, Gachancipá, Madrid, Mosquera, Nemocón, Sopó, Tabio, Tenjo, and Tocancipá.

It also applies partially to: Bogotá, Bojacá, Chipaque, Chocontá, Cogua, El Rosal, Cucunubá, Facatativá, Guasca, Guatavita, La Calera, Sesquilé, Sibaté, Soacha, Subachoque, Suesca, Tausa, Villapinzón, and Zipaquirá.

The Decree organizes its guidelines into five strategic components:

- Biodiversity conservation and climate change adaptation: promotes ecological connectivity, ecosystem restoration, and the protection of strategic areas.

- Integrated water resources management: strengthens the protection of aquifers, recharge areas, and surface and groundwater sources, prioritizing regional water security.

- Soil protection and conservation: establishes environmental criteria for urban expansion processes, preventing the degradation of land with high ecological and agricultural value.

- Sustainable infrastructure and green cities: requires new infrastructure projects to incorporate environmental criteria from the earliest stages of project planning, promoting sustainable mobility systems and nature-based solutions.

- Governance, information, and ancestral knowledge: incorporates mechanisms for interinstitutional coordination, open access to environmental information, and recognition of the traditional knowledge of Indigenous communities, particularly the Muisca people.

Key issues

- The Decree requires the updating of environmental mapping and watercourse buffer zones within specified timeframes.

- It promotes the ecological restoration of degraded areas and the protection of strategic ecosystems such as wetlands, Andean forests, and páramos.

- The Decree establishes a transition regime and clarifies that it does not alter vested legal rights or previously adopted planning instruments.

The environmental planning criteria must be incorporated into POTs and other planning instruments within twelve (12) months of the Decree’s effective date, beginning on May 29, 2026. During this period, priority will be given to environmental mapping, zoning, and the corresponding regulatory adjustments.

The Decree does not automatically modify projects that are covered by final administrative acts or environmental permits issued prior to its effective date, provided that such projects are carried out in accordance with the conditions established therein. However, these projects must assess related environmental risks and, where required by the competent authorities, adopt additional mitigation or compensation measures.

The municipalities identified in the Decree may face significant constraints on their autonomy to determine land use and guide their own development under the framework established by the Decree.

Property owners may face restrictions on land use and on the development of new urban projects within protected areas. Although ownership rights remain intact, owners may not freely develop, subdivide, construct on, exploit, or alter the use of their land when it is subject to environmental planning criteria. This is because the guidelines established by the Decree constitute binding criteria and rules for territorial and environmental planning and are considered rules of superior legal hierarchy within their respective spheres of competence.

The importance of protecting the Bogotá Savanna, its ecosystems, and its communities is beyond dispute. The legal issue, however, is whether the Decree maintains the constitutional balance between environmental protection of national significance and municipal autonomy.

The Constitution requires these two principles to coexist harmoniously. Therefore, the debate is not about the State’s authority to intervene, but rather whether certain provisions of the Decree exceed that authority and, in practice, displace decisions that the Constitution reserves to municipalities. This issue will likely be adjudicated by the courts, whose interpretation will ultimately define the boundaries between environmental powers and municipal autonomy.

Post-quantum digital signature and the reform of law 527 of 1999 in Colombia

By Daniel Peña Valenzuela

Introduction

Law 527 of 1999 marked a milestone in the regulation of electronic commerce in Colombia by recognizing the digital signature as a legal mechanism equivalent to the handwritten signature. This recognition consolidated trust in electronic transactions and granted evidentiary security to digital documents. The advent of quantum computing, however, poses an unprecedented challenge: the cryptographic algorithms underpinning digital signatures, such as RSA and ECC, may become vulnerable to the processing power of quantum computers. In this context, it is necessary to rethink the legal category of the digital signature and project regulatory reforms to ensure its validity in a post-quantum environment.

1. Digital signature under Law 527 of 1999

Law 527 establishes that the digital signature is an authentication mechanism based on public-key cryptography, guaranteeing the integrity and authenticity of electronic documents. The principle of technological neutrality allows any reliable method to be considered a digital signature, provided it meets security and functional equivalence standards. This principle must be reinterpreted in light of quantum risks, since legal validity depends on the technical robustness of the algorithms employed.

2. Quantum threat to digital signatures

Advances in quantum computing, particularly Shor’s algorithm, enable the factorization of large numbers and the resolution of discrete logarithm problems in polynomial time, directly undermining RSA and ECC. Likewise, Grover’s algorithm reduces the complexity of brute-force attacks on symmetric systems. These developments imply that current digital signatures may become vulnerable, weakening their evidentiary value in judicial and contractual processes.

3. Verifiable technical elements

The transition to a post-quantum environment requires the adoption of algorithms resistant to quantum attacks. The NIST (National Institute of Standards and Technology) selected between 2022 and 2024 algorithms such as CRYSTALS-Kyber for encryption and CRYSTALS-Dilithium for digital signatures. Similarly, ISO/IEC JTC 1 is working on international standards for post-quantum cryptography applicable to digital signatures. These verifiable technical elements form the basis upon which Colombian legislation must be reformed.

4. Need for reform of Law 527

The reform must explicitly recognize post-quantum algorithms as valid for digital signatures. It should also establish mechanisms for international interoperability with NIST and ISO standards, introduce the principle of technological resilience, and reinforce evidentiary guarantees to ensure that post-quantum digital signatures retain their functional equivalence with handwritten ones.

5. International comparison

In the European Union, the eIDAS 2.0 Regulation discusses the integration of quantum-resistant mechanisms. In the United States, NIST leads the standardization of post-quantum algorithms, directly impacting the validity of digital signatures. In Latin America, Colombia and Mexico have not yet explicitly incorporated the quantum threat into their legal frameworks, creating a regulatory gap and an opportunity for regional leadership.

Conclusions

The digital signature, as a legal category, faces a structural challenge in the quantum era. Reforming Law 527 is essential to recognize the post-quantum digital signature, adopt international standards, and guarantee the continuity of its functional equivalence. The post-quantum future does not eliminate the digital signature but requires its legal and technical transformation. Colombia must anticipate this transition to maintain legal certainty in electronic commerce and strengthen trust in digital transactions.

Gamification of Trading and Consumer Protection in Colombia: The Challenges of Using Foreign Platforms

By Daniel Peña Valenzuela, Partner Peña Mancero Abogados

Introduction

Gamification in trading has become a central strategy for digital platforms to attract and retain users. Through playful elements such as badges, rewards, leaderboards, and visual notifications, trading is transformed into a game-like experience. However, in Colombia, this practice raises serious consumer protection concerns, particularly when foreign platforms operate beyond the direct supervision of the Colombian Financial Superintendence.

This article examines the risks of gamified trading for Colombian consumers, highlights examples of international platforms such as Robinhood, eToro, and Binance, and proposes regulatory and cooperative mechanisms to mitigate digital manipulation in financial markets.

Dynamics of Gamification and Risks for Colombian Consumers

The logic of gamification in trading relies on behavioral stimuli designed to encourage frequent transactions. These stimuli, such as badges or visual rewards, create a sense of immediate achievement that can push users to repeat actions without properly assessing risks. A clear example is Robinhood in the United States, which was criticized for using digital confetti after trades, reinforcing emotional bias toward repeated trading.

Risks for Colombian consumers are significant. Gamification exploits behavioral biases such as loss aversion and the illusion of control, leading to impulsive decisions. Moreover, the extraterritoriality of platforms like eToro, based in Cyprus, or Binance, registered across multiple jurisdictions, makes direct oversight by the Colombian Financial Superintendence difficult. Finally, the information provided by these platforms often fails to meet the transparency standards required under Law 1480 of 2011, leaving consumers exposed.

Practical examples highlight these dynamics. Robinhood encourages high-frequency trading through simple interfaces and attractive visual cues. eToro promotes “copy trading,” where users replicate other investors’ strategies, potentially leading to uninformed decisions. Binance offers rewards and gamified token use, exposing consumers to volatile assets and increasing financial risk.

Conclusions

Gamified trading poses a challenge to consumer protection in Colombia. While it fosters financial inclusion, it also exposes users to manipulation and excessive risk. Needed measures include:

- International cooperation: bilateral and multilateral agreements to supervise foreign platforms.

- Warning protocols: clear digital messages about behavioral and financial risks.

- Financial education: programs teaching consumers to identify gamification techniques and their effects.

- Adaptive regulation: rules integrating consumer protection principles for digital and cross-border platforms.

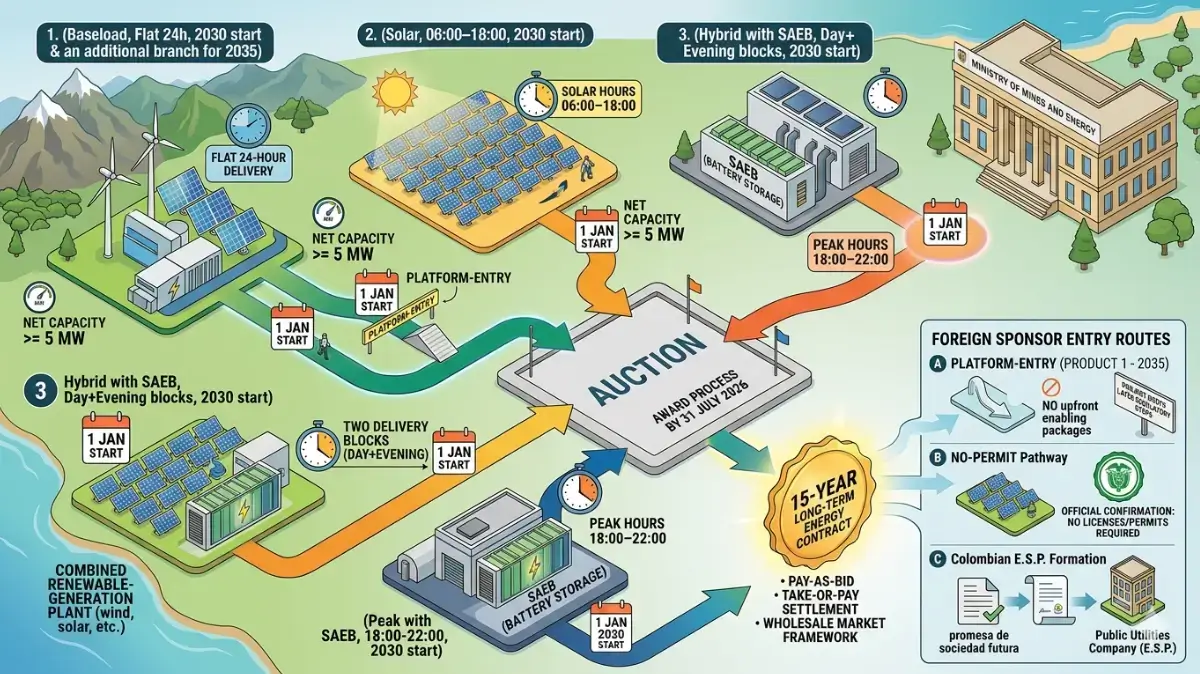

Alliott Global – Client Alert Colombia | 2026 Long-Term Renewable Energy Auction (Renewables & Storage): cross-border entry routes and near-term opportunities

Colombia’s Ministry of Mines and Energy has launched a new long‑term energy contracting mechanism, with the auction award process to be implemented no later than 31 July 2026.

Successful participants will enter into Long‑Term Energy Contracts with a 15‑year term starting from the contract obligations start date, under a pay‑as‑bid allocation design and a “take-or-pay‑contract” settlement approach within the wholesale market framework.

Contract pricing is based on the seller’s bid price plus the applicable regulated component (CERE), as provided in the auction rules

What is being auctioned?

The mechanism offers four (4) products differentiated by hourly delivery profile:

- Product 1 (Baseload): Flat delivery across 24 hours.

- Product 2 (Solar): Delivery aligned to solar hours 06:00–18:00 (12 hours).

- Product 3 (Hybrid): Two delivery blocks (day + evening) and participation requires the plant to include a SAEB (battery energy storage system) among its generation assets.

- Product 4 (Peak): Flat delivery 18:00–22:00 and energy must be delivered through a SAEB integrated as part of the generation assets.

The contracts will generally start on 1 January 2030. For Product 1, an additional auction will be held for contract starting on 1 January 2035.

Foreign sponsors: practical entry without an existing Colombia presence

For sell-side participation, the rules expressly allow foreign individuals and entities to participate through a Colombian participation structure, including a “company formation undertaking” (promesa de sociedad futura) to incorporate a Public Utilities Company (E.S.P.) domiciled in Colombia, which would assume the rights and obligations of a generator if awarded

Fast-track ways to participate (before 31 July 2026)

Two practical entry routes stand out for sponsors seeking a lighter upfront path into Colombia’s long-term contracting auction

- Product 1 with a 2035 start date: a straightforward “platform-entry” option. This track does not require the typical enabling packages at the time of participation, while the project still needs to meet the applicable regulatory steps over the course of development.

- “No-permit” projects: for smaller or lower-impact assets, sponsors may also pursue projects that can be supported with an official communication from the competent environmental authority confirming no environmental licenses, permits, authorizations are required.

Quick eligibility screen (minimum scale)

- Product 1: participation is available for: (i) new plants (renewables) with net effective capacity ≥ 5 MW; (ii) certain existing renewable plants meeting the applicable conditions, and (iii) new self-generators (autogenerators) with surplus ≥ 5 MW.

- Product 2: Reserved for new Solar PV plants and new solar self-generators with surplus, in each case with net effective capacity / surplus ≥ 5 MW

How Peña Mancero Abogados can support Alliott member clients

- Auction-entry structuring for foreign sponsors (E.S.P. or “promesa de sociedad futura”) and governance documentation.

- Fast eligibility screen identifying the simplest route (Product 1–2035 or “no‑permit” environmental pathway projects and the minimum capacity fit (≥ 5 MW where applicable)

- Auction representation as a client counsel and attorney‑in‑fact for filings, platform steps and bid process coordination with the auction operator.

- If awarded, support the auction‑operator mandate agreement for centralized contract/guarantee administration and the required market registrations and ongoing energy market compliance to operate and settle under Colombian rule.

Contact

Gabriela Mancero – Partner | gabrielam@pmabogados.co

Mauricio Torres – Energy & Infrastructure | mauriciot@pmabogados.co

Contracts for Difference (CFDs): an opportunity for the energy sector

By Gabriela Mancero for the Minas Petróleos & Energía Bar Association

In the Colombian context, Contracts for Difference (CFDs) can be a key tool for encouraging investment in renewable energy and stabilizing electricity prices.

Regulation of CFDs in Colombia

In financial terms, a Contract for Difference (CFD) is a financial derivatives contract. It can be entered into on a number of different products. The largest markets for CFD financial products are currency and interest rate swaps. In derivative contracts, the actual asset, in financial terms, the underlying asset, is not traded. The transaction is purely financial. In CFD contracts, an agreement is established between two parties to exchange payments based on the price of an underlying asset.

The Banco de la República de Colombia is the regulatory authority for foreign exchange matters. As such, it is responsible for supervising the Colombian cross-border derivatives market and the local derivatives market related to foreign exchange transactions. CFDs are generally defined as derivative products that allow investors to take a position on changes in the value of an underlying asset.

In Colombia, CFDs are atypical contracts, not regulated by law. Despite this nature, the Banco de la República has classified CFDs by interpretation as financial derivatives. Investments can be made with both local and foreign agents authorized as so-called authorized foreign agents or online dealers or market makers, as permitted by local regulations.

Foreign agents authorized to carry out derivative transactions with Colombian residents are those non-domiciled entities that have carried out such transactions in the immediately preceding year for a nominal value exceeding USD 1,000,000,000. Despite this requirement, Colombian residents, and not a government entity in Colombia, are responsible for properly assessing compliance with this requirement by foreign agents.

In derivative contracts, the actual asset, in financial terms: the underlying asset, is not traded. The transaction is purely financial.

In Colombia, CFDs can be used to provide stable long-term prices for renewable energy producers, protecting them from the volatility of the electricity market. These contracts allow producers to sell their energy at an agreed fixed price, while the State or a regulatory entity assumes the risk of market fluctuations. It is the movements in the price of the underlying asset that trigger payments between the parties to the contract without the actual asset changing hands, i.e., without physical delivery or transfer of ownership of the electricity. These transactions are carried out on margin, which involves the periodic delivery of money to the agent so that they can continue trading. CFDs can also be used to protect consumers from high electricity prices.

Here are some international examples of the successful use of CFDs in renewable energy:

- The United Kingdom has been a pioneer in the implementation of CFDs for renewable energy. In the latest round of auctions in 2017, two offshore wind projects were awarded CFD contracts at £57.50/MWh (€64.10/MWh), representing a 50% reduction in the costs of contracts awarded 30 months earlier.

- The European Commission has proposed a reform of the electricity market that includes the implementation of bidirectional CFDs for new renewable electricity projects and nuclear power plants. These contracts allow the state to compensate the producer if market prices fall below an agreed threshold and to capture the excess revenue if prices exceed that threshold.

- In Spain, CFDs are used as part of renewable energy auctions to ensure stable long-term prices for renewable energy producers. These contracts are awarded through competitive auctions, where producers bid the lowest price at which they are willing to sell their energy. These examples show how CFDs are increasingly seen as the preferred method for incentivizing investment in low-carbon projects and new technologies, leading to a two-way CFD model being the recommended market mechanism for contracts to be signed in the Colombia Offshore Wind Round led by the National Hydrocarbons Agency (ANH).

When designing CFDs, regulators typically pursue two broad objectives: first, to incentivize investment in renewables in line with the policy objectives of their development plans, and second, to integrate renewables into energy markets with as little distortion as possible. At the same time, the development of the energy system must follow the principles of security of supply and cost minimization. Contracts for Difference can play a crucial role in Colombia’s energy transition by providing price stability and encouraging investment in renewable energy. With an appropriate legal framework and transparent procedures, CFDs can help Colombia achieve its sustainability and energy security goals.

Crypto-asset regulation in colombia: recent trends

The regulation on crypto-assets is a relevant index to determine the digital business climate in a country. Like any emerging technology, its early adoption in a market and adequate regulation can be an important step in the digital transformation processes in companies, the government and support digital entrepreneurship. The efficiency and data decentralization of blockchain and cryptocurrencies generate disruptive effects in certain markets and may also create concern about eventual illegal activities deriving from the technology’s relative anonymity.

In Colombia, several public entities have issued regulation and opinions on crypto-assets. This is precisely the first trend that we want to highlight. In Colombia there is a diversity of public entities that have touched upon different legal issues related to crypto-assets, namely: financial, exchange, tax, commercial, compliance and contractual issues, among others.

The following is a list with the main existing regulation and opinions:

(a) Financial Superintendence, Chapter XVIII External Circular Letter No. 041 of 2015;

(b) Decree 2555 of 2010.

(c) Regulatory Decree 1068 of 2015 (article 2.17.2.4.1.1);

(d) External Resolution No. 8 of May 5, 2000;

(e) External Resolution No. 1 of May 25, 2018;

(f) External Circular Letter No. DODM-144 of September 14, 2018;

(g) External Circular Letter No. DECIP-83 of August 27, 2021;

(h) Central Bank Opinion No. JDS-03409 of February 16, 2011;

(i) Central Bank Opinion No. JDS-19704 of September 12, 2016;

(j) Central Bank Opinion No. C19-110904 of June 21, 2019;

(k) Central Bank Opinion No. C21-70969 Q21-4417 of December 9, 2021;

(l) Financial Superintendence Opinion No. 2020079520-001 of May 15, 2020.

This is an effect of the transversal use of crypto-assets in different economic sectors and for different activities. However, if greater legal certainty is sought, the government could adopt a public policy document defining the vision and direction of the relationship between the public and the private sectors in relation to these digital assets.

In general, the Colombian authorities agree on the following characteristics related to crypto-assets as a basis for their regulation in each legal field and to determine the risks of the crypto title-holders who trade these intangible assets:

- Crypto-assets are not currency, as the only monetary and account unit that constitutes a legal tender and means of payment with unlimited release power, is the Colombian peso issued by the Central Bank of Colombia (bills and coins);

- Crypto-assets are not money for legal purposes;

- Crypto-assets are not a currency, since it has not been recognized as a currency by any international monetary authority nor is it supported by central banks;

- Crypto-assets are not cash or cash equivalent;

- There is no obligation to receive crypto-assets as a means of payment;

- Crypto-assets are not financial assets or investment property in accounting terms;

- Crypto-assets are not securities, so their mention as such or assimilation should be avoided.

The above characteristics have been consistently upheld by different Colombian government documents and denote an interpretation of intangibles that is always based on traditional notions of assets.

Crypto-assets have been defined in Colombia as intangible assets and therefore are likely to be contributed to the capital of corporations, provided that (i) they comply with accounting laws and secondary rules and legal regulations; and (ii) that the partners approve their appraisal. Based on these arguments, the Colombian government expressly affirmed a change in its doctrine, confirming that shareholders can contribute crypto-assets in the form of a contribution in kind. The foregoing, subject to a series of requirements and recommendations, opens the possibility of incorporating crypto-assets as part of the incorporation of companies in Colombia.

Colombian residents who have crypto-assets as part of their assets must declare them in their annual income tax returns. The value for which they must be declared will be for their equity value, either as an intangible asset (investment) or inventory.

On the accounting side, it is recommended that a separate unit of account be created for the recognition, measurement and disclosure of transactions and other events or occurrences that are related to cryptocurrencies, which could well be called “crypto-assets” or “virtual assets”.

If the crypto-assets are traded in a foreign currency, the value of the assets in foreign currency is estimated in national currency at the time of their initial recognition at the official exchange rate, less credits or payments measured at the same official exchange rate of the initial recognition.

Colombian residents who have equipment, resources and work that are integrated into the crypto mining activity, allowing them to obtain virtual currencies in exchange for the services provided in the network and/or by way of commissions, receive taxable income in Colombia, by virtue of the aforementioned criteria. Likewise, it is clear that resident individuals and national companies are taxed not only on their income from a national source but also from a foreign source income and on their assets owned in the country and abroad. From the equity point of view, as long as these coins correspond to intangible assets, capable of being valued, they form part of the equity and can lead to the obtaining of (presumptive) income.

For instance, the purchase and sale of real estate with payment through crypto-assets is an exchange of an asset whose payment will be made through the delivery of an intangible asset. The tax obligations associated with income tax will be those derived from the execution of the exchange contract. Carrying out the exchange will affect the assets of the party delivering the crypto-asset; the payment of the price will generate an equity decrease due to its disposal. On the other hand, depending on the real estate valuation, seller may increase its assets by carrying out the respective exchange, or equate the equity value of the crypto-asset delivered. Consequently, the party delivering the crypto-asset must determine the equity value of said asset, and analyze whether, on the occasion of the exchange, an income for the difference between the tax cost of the asset and the value of its disposal was obtained. The payment of the property through crypto-assets may represent an increase in equity in the head of the property seller if the equity value of the crypto-asset is higher than that of the real estate. The capital increase must be reported in that party’s accounting and income tax return. To the same extent, the real estate seller must determine the equity value of said property, and verify if, on the occasion of the exchange, an income for the difference between the fiscal cost of the real estate and the value of the sale was obtained. The parties must comply with the provisions of the Colombian Tax Statute for the purpose of determining the minimum prices for the sale of the goods subject to the exchange.

As in other jurisdictions, Colombia is no exception for crypto-assets being used in criminal activities. Cases of criminal use, fraud and the use of crypto-assets for payments related to computer attacks and ransomware as well as for payments related to extortion are becoming more frequent. Crypto-assets can also be used as instruments for money laundering, terrorist financing and other criminal activities, in view of which the administrators of the companies that participate in the crypto-asset market must deploy: i) the maximum due diligence in the knowledge of the ends of the operation (including associates, employees, clients, contractors and suppliers, and their final beneficiaries), in regards to the prevention of ML/TF; and, ii) the diligence that a businessman in good faith would take into account to prevent the phenomenon of asset laundering or money from the public being illegally collected or any other damage to the public or private interest being generated through such company. Those who carry out operations with crypto-assets decide in a responsible, conscious and autonomous manner, at their own expense and risk, to assume the possible losses that could be derived from this type of transaction.

The difficulty of clearly defining crypto-assets has been used by criminals to deceive investors and to carry out illegal collection of funds and Ponzi schemes with business models and strategies that can only be carried out by financial entities authorized by the Colombian government.

The growth of the crypto-asset market, in particular cryptocurrencies, depends on the ability of crypto-assets being used in many activities. So, while there is need for a clear regulatory framework that allows measuring risks, it is also important that absolute prohibitions or regulatory disincentives disappear.

In the past two years, a bill that regulates the relationship between wallets, exchanges and platforms in relation to crypto assets has advanced for approval in the Colombian Congress. In the first place, this proposed legislation proposes a series of definitions, among others, the following:

- Wallets: These are the virtual media in which the public and private encryption keys are stored.

- Crypto-assets Exchange Services: these are the following services: (i) Administration of crypto-assets exchange platforms. (ii). Provision of custody and/or storage services for crypto assets. (iii). Exchange or transfer between crypto-assets and fiat currency, or between one or more crypto-assets. (iv). The supplementary or analogous services related to sections i, ii and iii above.

- Crypto Asset Exchange Platform (PIC): These are computer applications or interfaces, internet pages or any other means of electronic or digital communication through which the Crypto-asset Exchange Services are provided.

- Crypto-asset Exchange Service Provider: It is a national business entity or a branch of a foreign company, in charge of operating, managing and guaranteeing the operation of the PIC, registering with the Chamber of Commerce of its main domicile and responsible for compliance with the obligations.

- Unique Registry of Crypto-asset Exchange Platforms (RUPIC): It is an electronic public registry managed by the Chambers of Commerce whose objective is to allow anyone to access the information published in said registry, and to verify that the Service Providers of Crypto-assets Exchange as holders are duly registered.

- PIC Operations Manual: Document that contains the requirements and internal parameters of the PIC for the provision of Crypto-asset Exchange Services.

As a principle of interpretation of the crypto-asset market, it is established in the draft bill that crypto-assets are negotiable directly by their owners. The operation of the different crypto assets, their rules belong to the private sphere of the users, who, based on the principles of free market and free competition, must seek to be informed about the risks inherent in trading with assets of any kind.

The Crypto-asset Exchange Service Providers, Colombian or foreigners, must comply with the following requirements:

- Be incorporated as a commercial company domiciled in Colombia or as a branch of a foreign company, and be duly registered in the Colombian mercantile registry.

- Include as the exclusive corporate purpose the performance of activities classified as Crypto-asset Exchange Services.

- Establish and maintain a computer security program that ensures the availability and functionality of its computer systems, protecting said systems and all information stored in them, from unauthorized access, use and manipulation, the foregoing in accordance with the instructions that for this purpose imparted by the Ministry of Information Technology and Communications.

- Adopt control measures aimed at detecting and preventing money laundering and terrorist financing.

- Register in the Special Register for Crypto-assets Service Providers before the Chamber of Commerce of the entity’s main address, indicating the web domain and the information determined by the Ministry of Information and Communication Technologies.

- Report to the Financial Information and Analysis Unit the information that is required in compliance with money laundering regulations.

- Comply with the Colombian personal data protection regulations.

- Implement KYC and customer Due Diligence measures.

- Have an Operations Manual for the operation of the PICs that it manages, approved by the Ministry of Information Technologies and Communications.

According to the proposed bill, the Crypto-assets Exchange Service Providers are prohibited from:

- Offering or paying consumers interests or any other return or monetary benefit for the balance that they accumulate over time or maintain or for any operation directly or indirectly related to the exchange that they carry out with crypto-assets.

- Transferring under any title, lend or encumber crypto-assets or any other resource owned by consumers, stored by the Crypto-asset Exchange Service Provider, without the express authorization of the consumer.

- Developing any kinds of commercial network or multi-level marketing activity with crypto-assets, as well as their financial intermediation. Likewise, the administrators or service providers of crypto-asset exchange platforms may not allow the commercial distribution of crypto-assets to be carried out on their platforms through network or multi-level marketing activities or similar.

- Refraining from carrying out any conduct that leads to the massive and regular collection of funds from the public that additionally implies the absence of consideration in present or future goods or services that justify it or, even if such consideration exists, does not have a reasonable financial explanation.

The model proposed in this draft bill does not comprehensively regulate the different legal aspects of crypto assets. The relationship between some of the agents in the ecosystem can set aside a holistic vision that is necessary to obtain the benefits of intelligent regulation. It is not clear if the Financial Regulation Unit of the Colombian government agrees with the content of this bill.

To sum up, in Colombia there is a regulatory trend that has been transforming from a prohibition on the use of crypto-assets towards a vision more associated with the risks inherent in the market for these digital assets. The regulation remains disperse since different Colombian public entities with market supervision and surveillance functions have issued rules and opinions related to accounting, tax, contractual, exchange and financial issues, among others. An effective coordination between the different public entities that regulate crypto-assets is necessary to achieve legal certainty and stimulate the use of these digital assets as well as to generate a business environment that allows attracting investment. It is necessary to wait and see if the draft bill that is in progress becomes law so that wallets, exchanges and crypto-asset offering platforms in particular, are regulated more specifically in terms of their registration and duties as well as their liability towards consumers and users of crypto-assets.

New regulation on electronic payroll In Colombia

By: María del Pilar Duplat M. – Peña Mancero Abogados

The Colombian tax authority (DIAN by its Spanish acronym) issued resolution 13 of February 11, 2021 regulating the implementation of the electronic payroll system (the “Electronic Payroll Resolution” or the “Resolution”).

Who must submit the electronic payroll to DIAN?

Income taxpayers that are employers or that make payments due to legal or regulatory relationships or that make pension payments, and require to support said costs and deductions in their tax returns.

On a monthly basis, the aforementioned subjects must submit to DIAN a payroll supporting document for its approval or correction.

What is the payroll supporting document?

The electronic payroll supporting document is the document that shows all labor-related payments made by the employer. This document must contain the following information for its creation, transmission and approval by DIAN:

- Expressly indicate that it is an electronic payroll supporting document.

- Employer complete name of the individual or entity, ID Number or tax id number.

- Complete name(s) and ID of the person who receives the payment.

- The Unique Code Number of the Supporting Document of the electronic Payroll (CUNE by its initials in Spanish).

- Internal consecutive number granted by the subject obliged to submit the electronic payroll.

- Contents and amounts of the accrued value of payroll pursuant to the Technical Appendix to the Electronic Payroll Resolution.

- Contents and amounts of the deducted sums from the payroll pursuant to the Technical Appendix to the Electronic Payroll Resolution.

- Total amount resulting from the difference between the total accrued payroll payments minus the total deducted sums from the payroll payments.

- The contents of the Technical Appendix as provided in article 20 of the Electronic Payroll Resolution, regarding the information and contents contained herein.

- The form of payment of the payroll per the Technical Appendix to the Payroll Resolution.

- Date and time of creation of the document.

- Digital signature of the Subject who pays the Payroll in accordance with the DIAN’s requirements of authenticity and integrity of the signature.

- Complete name and ID or tax id number of the software supplier and identification of the software.

When do I have to submit the electronic payroll to DIAN?

The electronic payroll supporting document must be issued and sent to DIAN on a monthly basis, ten (10) days after its creation or issuance.

As of when must the electronic payroll be implemented?

- Implementation Calendar for subjects per the number of employees

| Group | Beginning date of the enabling of the electronic payroll data processing system | Maximum date to start the issuance and transmission of the electronic payroll payment support document and the electronic payroll payment support document adjustment notes. | Range in relation to the number of employees

|

|

| From | Until | |||

| 1 | May 31st, 2021 | July 01, 2021 | More than 251 | |

| 2 | August 01, 2021 | 101 | 250 | |

| 3 | September 01, 2021 | 11 | 100 | |

| 4 | October 01, 2021 | 4 | 10 | |

| 5 | November 01, 2021 | 2 | 3 | |

| 6 | December 01, 2021 | 1 | ||

- Permanent Implementation Calendar

The obliged subjects will have a term of two (2) months from the date in which they make the payroll payments to carry out the enabling of the service and proceeding to transmit the supporting documents of the electronic payroll and its adjustment notes.

The remaining subjects must issue the supporting payroll document and their adjustment notes to request the costs and deductions of the income tax and the VAT deductible taxes, when applicable.

- Implementation calendar for subjects not obliged to issue electronic sales invoices

Subjects not obliged to issue electronic sales invoices must start the enabling of the electronic data payroll service on March 31, 2022; and they must issue and send the supporting document of the payment of the electronic payroll and their adjustment notes, no later than May 31, 2022.

How do I issue the electronic payroll documents?

The enabling procedure is the one that is developed within the electronic invoicing system which must have the function to issue the electronic payroll supporting document pursuant to DIAN’s requirements.

The enabling procedure must be carried out before the date when the subjects must start with the implementation and the term when they must submit the monthly electronic payroll.

If you have further inquiries regarding this new regulation, please do not hesitate to contact us at: info@pmabogados.co

Why a due diligence process may become a nightmare in Colombia?

Strong institutions with reliable databases available to the public are key when carrying out a due diligence process. In most cases, information provided by the target is insufficient and not always accurate. This means that attorneys must be creative in order to look for the right information in the right places.

Here are some examples of what can go wrong if a due diligence process is not properly handled:

- Real estate is tricky in Colombia, especially when you acquire assets or companies with rural real estate. Many attorneys focus on making sure that the “owner” of the land or property is duly recorded with the Real Estate Registry without realizing there is so much more! For instance: (i) determining whether the area has oil & gas or mining licenses that would create compulsory easements or eventually hinder its use; (ii) determining whether there are environmental restrictions such as being part of a national park, a protected wetland or a forest; (iii) verifying whether the land was formerly owned by communities or people who had to give it up because of armed groups’ pressure and are now subject to restitution proceedings; (iv) confirming that the land is not in fact a barren land that someone occupied as, regardless of time lapsed, it will continue to be State-owned and not subject to transfer.

- The Superintendence of Corporations recently issued a new regulation introducing stricter rules for anti-money laundering and terrorism financing. We cannot hide that Colombia has individuals and companies involved in such activities that do business in creative manners so as to disguise the true origin of their funds. A proper investigation during due diligence should include examining who the beneficial owners of the target are and searching not only the standard international OFAC and similar lists but also carrying out a full search of local media publications and other more informal sources of information.

- Latin American countries keep facing more and more corruption scandals. Colombia is not the exception. Doing business with relatives, partners and close friends of politically exposed parties can be risky. A proper due diligence should involve requesting full disclosure not only from all sellers but also from the target’s main stakeholders. Regulatory standards can be found in the Colombian anti-corruption statute.

- Unlike most Latin American countries, Colombia’s foreign exchange regulation imposes strict reporting obligations concerning foreign-currency-related operations such as foreign investment, receiving or granting loans from/to foreign residents, granting securities abroad, imports and exports. Non-compliance with such obligations may derive in huge fines to be imposed either by the Superintendence of Corporations or by the tax authority (DIAN). To avoid such liability, due diligence should include reviewing all the above foreign exchange transactions including: timely filing of reports to the Central Bank; correct reporting of each transaction; requesting an up-to-date report from the Central Bank to obtain information on all reported items.

- When searching for the history of land, corporations, litigation, property and any other asset that is subject to public record, one must be careful in Colombia. Government agencies are not always up-to-date and technology tends to be basic when it comes to search engines. There are entities and courts who simply do not provide such service to the public so not being able to complete an independent verification of the target’s records is common.

Being able to distinguish between what a “deal breaker” is and what not requires a thorough understanding of the risks involved and their eventual effects. For example, if a mining license does exist on the target’s land, a deal breaker would be not being able to use the land at all because of a compulsory easement that would prevent you from carrying out any activity whatsoever and that land being essential and of great value to the business you are acquiring. Otherwise, you may still negotiate such liability being properly disclosed in the “Disclosure Schedule” of the purchase agreement and establishing an escrow or taking any other measure to tackle loss if occurring. The same thing cannot be said when there are findings concerning money laundering or corruption charges. The risk involved in such situations would need to be measured in a very conservative manner as effects would not only involve economic consequences but eventual imprisonment.

Peña Mancero Abogados is publishing a series of high-level articles on M&A activity in Colombia. This article is for information purposes only and does not constitute legal advice. If you require further information, please contact Gabriela Mancero (info@pmabogados.co)

CAUSE FOR DISOLUTION OF COMPANIES DUE TO NON-COMPLIANCE WITH THE HYPOTHESIS OF CONTINUING BUSINESS

By: Daniel Salazar López

The current political, social and economic crisis as a result of COVID-19 outbreak, led many companies and branches of foreign companies to enter into a cause for dissolution for losses or accumulated losses, some of them overcame the cause for dissolution while others had to be liquidated.

Until recently, in Colombia a company entered into a cause for dissolution when it had losses or accumulated losses which resulted in a decrease in equity below 50% of its subscribed capital. If this cause for dissolution was not solved within a 2 year period, the company had to be liquidated. Nevertheless, Law 2069 of 2021 (Entrepreneurship Law) eliminated this cause for dissolution and liquidation of companies in Colombia, and introduced a new cause for dissolution, the non-compliance with the hypothesis of continuing business. This is a step forward in corporate matters, since the cause of losses caused confusion, firstly taking into account that companies at the beginning of their economic activity generated high costs that prevented them from having profits at the end of the fiscal year, and therefore entering into grounds for dissolution; previously, at the closing of each fiscal year, the cause for dissolution was warned of and could be enervated within the established term, now it is imperative that the administrators of a company intervene more thoroughly on the hypothesis of continuing business.

The hypothesis of continuing business provides that provides that at the end of the fiscal year, a company must evaluate its financial statements to determine whether it has the capacity to continue operating. Therefore, when the highest corporate body analyses and evaluates the financial statements prepared under the hypothesis of continuing business, and it is observed that there is a detriment to the company’s assets and that this casts doubt on the continuity of the company’s continuing business[1], the company will be subject to dissolution.

If your company has an International Financial Reporting Standard (IFRS) accounting framework, the management under IFRS will assess the entity’s ability to continue with its businesses, which underlines the importance of preparing financial statements for the fiscal year 2020 in the current business environment. On the other hand, the companies that were subject to dissolution due to losses before the entry into force of Law 2069, such cause was suspended by virtue of Decrees 560 and 772 of 2020, while the companies are recovering in the midst of the crisis generated by COVID-19. It is worth mentioning that such suspension is extended to Law 2069 until the end of the term of such decrees, i.e., until April 2022.

In view of the foregoing, when the administrator notices in the financial statements of the fiscal year that the hypothesis of continuing business is not complied with, the administrator must summon the highest corporate body to inform in a documented manner such situation, so that the highest corporate organ of the company declares that the company has entered into dissolution grounds and therefore measures must be taken to continue with the business or to liquidate the company. It is important to highlight that when the company enters into a cause for dissolution, the administrators must abstain from carrying out new operations different from the ordinary course of business of the company. In case of non-compliance with the duty to inform the respective highest body by the administrator, the administrator shall be jointly and severally liable for the damages caused to the members of the Company or third parties. In assessing whether continuing business situation is appropriate, the management shall consider all available facts about the future, which shall cover at least, but not be limited to, the next twelve (12) months from the reporting date.

The following situations are considered as non-compliance with the continuing business hypothesis:

- Liquidity risk

- Legal claims of significant contingencies.

- Low quality condition of the company’s products or services.

- Termination of contracts with significant customer and suppliers.

- High consecutive borrowing to invest in long-term business.

- Financial losses due to failure to meet contractual payment obligations.

- Labor strikes that have a significant impact on the company´s result.

- If there are delay in the payment of liabilities with banks, payroll or dividends.

Thus, if the company has a history of profitable operations and it´s positive cash flow projections indicate appropriate access to financial resources, it can be concluded that the use of the hypothesis of continuing business is appropriate. Now, it is imperative to prepare the financial statements for the fiscal year, including the trial or periodic financial statements, and the concept issued by the accountant will become more relevant since the highest corporate body will determine the viability in the short and medium term (12 months), avoiding deterioration in the common pledge of the creditors and in the equity of the associates. If, on the contrary, there is an uncertainty in the operations of the ordinary course of business of the company, and it isn´t possible to cover it within the following twelve months, the cause of non-compliance with the hypothesis of continuing business is configured and the company must proceed with its dissolution and liquidation. The proposal of this new cause seeks to protect the contingencies derived from the state of emergency due to COVID-19.

[1] Consejo Técnico de la Contaduría Pública Radicado 2018-095, del 2 de febrero de 2018

Data Protection & Privacy

Autor: Daniel Peña Valenzuela

Editorial: European Lawyer

Categoría: Data Protection, European & EU Law

Año de Edición: 08 Nov 2016

Formato: Libro Impreso

Número de páginas: 1124

ISBN: 9780414057821

The number of jurisdictions with laws on data protection and privacy is still on the rise and the interest in the area of data protection and privacy has never been greater. The book aims to create a single starting point of reference for businesses, data protection officers, advisers and legal professionals involved in data protection and privacy. This third edition of Data Protection & Privacy – Jurisdictional Comparisons serves as an indispensable reference guide on the data protection and privacy laws in over 40 countries from six continents.

Written by expert local practitioners, with deep experience in the field of data protection and privacy, every chapter contains an overview of the key elements and principles of the data protection and privacy law framework in the relevant jurisdiction as well as the latest developments and trends. Because each chapter follows the same Q&A structure, readers can conduct quick comparisons between the various legal regimes.

Contents

1. Legislation

2. Data protection authority

3. Legal basis for data processing

4. Special rules

5. Data quality requirements

6. Outsourcing and due diligence

7. International data transfers

8. Information obligations

9. Rights of individuals

10. Security of data processing

11. Data protection impact assessments, audits and seals

12. Registration obligations

13. Data protection officer

14. Enforcement and sanctions

15. Remedies and liability

Jurisdictional coverage

1. Argentina – Marval, O’farrell & Mairal

2. Australia – Gilbert + Tobin

3. Austria – Preslmayr Rechtsanwälte Og

4. Belgium – Covington & Burling Llp

5. Brazil – Felsberg Advogados

6. Bulgaria – Djingov, Gouginski, Kyutchukov & Velichkov

7. Canada – Osler

8. Chile – Palma & Palma Abogados

9. Colombia – Peña Mancero Abogados

10. Costa Rica – Thompson Abogados

11. Czech Republic – Havel, Holásek & Partners S.R.O.

12. Denmark – Beck – Bruun

13. EU – Covington & Burling Llp

14. EU Institutions & Bodies – European Commission

15. Germany – Covington & Burling Llp

16. Hong Kong – Deacons

17. Hungary – Oppenheim Law Firm

18. India – Vaish Associates Advocates

19. Ireland – Mason Hayes Curran

20. Israel – Vigal Arnon & Co

21. Italy – NCTM

22. Japan – Atsumi & Sakai

23. Lithuania – Valiunas Ellex

24. Luxembourg – Arendt & Medernach SA

25. Malaysia – Christopher Lee Ong

26. Malta – GVTH Advocates

27. Mexico – Laurant Abogados

28. Morocco – Hajji & Associes

29. Netherlands – Vondst Advocaten

30. Poland – Soltysinski Kawecki & Szlezak

31. Portugal – Coelho Ribeiro E Associados

32. Romania – Nestor Nestor Diculescu Kingston Petersen

33. Singapore – Wongpartnership Llp

34. Slovakia – Havel, Holásek & Partners S.R.O

35. Slovenia – Rojs, Peljhan, Prelesnik & Partnerji

36. South Africa –Adams & Adams

37. South Africa – Lee & Ko

38. Spain – Garrigues

39. Sweden – Mannheimer Swartling Advokatbyrå Ab

40. Switzerland – Lenz & Staehelin

41. Taiwan – Lee And Li, Attorneys-At-Law

42. Turkey – Elig

43. Uae – Al Tamimi & Company

44. Uk – Covington & Burling Llp

45. Usa – Covington & Burling Llp

International Joint Ventures (2013)

GABRIELA MANCERO,

JOINT VENTURE IN COLOMBIA, PAGS 91-102,

OBRA: INTERNATIONAL JOINT VENTURES, A GUIDE OR U.S. LAWYERS (INTERNATIONAL JOINT VENTURES/MERGERS AND ACQUISITIONS COMMITTEE)

CHICAGO, AMERICAN BAR ASSOCIATION,

AÑO: 2013.

This publication is part of a series of works published by the international Mergers & Acquisitions Subcommittee to assist business lawyers in advising clients in international transactions. The focus of this publication is on bilateral joint ventures between US and overseas coventurers.

This publication is part of a series of works published by the international Mergers & Acquisitions Subcommittee to assist business lawyers in advising clients in international transactions. The focus of this publication is on bilateral joint ventures between US and overseas coventurers.

In providing a framework for considering issues particular to a jurisdiction’s legal system and culture, the Task Force has crafted a flexible but relatively uniform method of how to think about issues particular to international joint venture. The result is a reference work that is intended to serve as a starting point from which to map out effective agreements.

Areas of practice

Litigation

National and International Arbitration

International Contracting

Corporate or Company Law

Mergers and Acquisitions

Commercial Law

Intellectual Property

Competition Law

International Cooperation and Non-Profit Entities

Foreign Investment

Immigration Law

Tax law

Exchange Law

Mining Law

Energy Law

Information Technologies and Telecommunications

Protection of Personal Data and Privacy

Consumer Protection

Labor Law and Social Security

Real Estate and Urban Planning Law

Awards

")

")

Memberships