Newsletter Jun 2026

Decree 0545 of 2026, Issued May 29, 2026

“Whereby guidelines for the environmental planning of the Bogotá Savanna are established”

The National Government issued Decree 0545 of 2026 for the purpose of establishing guidelines for the environmental planning of the Bogotá Savanna, pursuant to the mandate set forth in Article 61 of Law 99 of 1993, which recognizes this region as an area of national ecological interest.

These guidelines constitute binding environmental planning criteria and rules of superior legal hierarchy that must be incorporated by territorial entities and considered by environmental authorities in the exercise of their respective powers.

The Decree applies to Bogotá D.C., the municipalities that comprise the Bogotá Savanna, and the authorities and entities responsible for territorial planning and land-use management.

The Bogotá Savanna encompasses 31 municipalities. The Decree applies in its entirety to: Cajicá, Chía, Cota, Funza, Gachancipá, Madrid, Mosquera, Nemocón, Sopó, Tabio, Tenjo, and Tocancipá.

It also applies partially to: Bogotá, Bojacá, Chipaque, Chocontá, Cogua, El Rosal, Cucunubá, Facatativá, Guasca, Guatavita, La Calera, Sesquilé, Sibaté, Soacha, Subachoque, Suesca, Tausa, Villapinzón, and Zipaquirá.

The Decree organizes its guidelines into five strategic components:

- Biodiversity conservation and climate change adaptation: promotes ecological connectivity, ecosystem restoration, and the protection of strategic areas.

- Integrated water resources management: strengthens the protection of aquifers, recharge areas, and surface and groundwater sources, prioritizing regional water security.

- Soil protection and conservation: establishes environmental criteria for urban expansion processes, preventing the degradation of land with high ecological and agricultural value.

- Sustainable infrastructure and green cities: requires new infrastructure projects to incorporate environmental criteria from the earliest stages of project planning, promoting sustainable mobility systems and nature-based solutions.

- Governance, information, and ancestral knowledge: incorporates mechanisms for interinstitutional coordination, open access to environmental information, and recognition of the traditional knowledge of Indigenous communities, particularly the Muisca people.

Key issues

- The Decree requires the updating of environmental mapping and watercourse buffer zones within specified timeframes.

- It promotes the ecological restoration of degraded areas and the protection of strategic ecosystems such as wetlands, Andean forests, and páramos.

- The Decree establishes a transition regime and clarifies that it does not alter vested legal rights or previously adopted planning instruments.

The environmental planning criteria must be incorporated into POTs and other planning instruments within twelve (12) months of the Decree’s effective date, beginning on May 29, 2026. During this period, priority will be given to environmental mapping, zoning, and the corresponding regulatory adjustments.

The Decree does not automatically modify projects that are covered by final administrative acts or environmental permits issued prior to its effective date, provided that such projects are carried out in accordance with the conditions established therein. However, these projects must assess related environmental risks and, where required by the competent authorities, adopt additional mitigation or compensation measures.

The municipalities identified in the Decree may face significant constraints on their autonomy to determine land use and guide their own development under the framework established by the Decree.

Property owners may face restrictions on land use and on the development of new urban projects within protected areas. Although ownership rights remain intact, owners may not freely develop, subdivide, construct on, exploit, or alter the use of their land when it is subject to environmental planning criteria. This is because the guidelines established by the Decree constitute binding criteria and rules for territorial and environmental planning and are considered rules of superior legal hierarchy within their respective spheres of competence.

The importance of protecting the Bogotá Savanna, its ecosystems, and its communities is beyond dispute. The legal issue, however, is whether the Decree maintains the constitutional balance between environmental protection of national significance and municipal autonomy.

The Constitution requires these two principles to coexist harmoniously. Therefore, the debate is not about the State’s authority to intervene, but rather whether certain provisions of the Decree exceed that authority and, in practice, displace decisions that the Constitution reserves to municipalities. This issue will likely be adjudicated by the courts, whose interpretation will ultimately define the boundaries between environmental powers and municipal autonomy.

Post-quantum digital signature and the reform of law 527 of 1999 in Colombia

By Daniel Peña Valenzuela

Introduction

Law 527 of 1999 marked a milestone in the regulation of electronic commerce in Colombia by recognizing the digital signature as a legal mechanism equivalent to the handwritten signature. This recognition consolidated trust in electronic transactions and granted evidentiary security to digital documents. The advent of quantum computing, however, poses an unprecedented challenge: the cryptographic algorithms underpinning digital signatures, such as RSA and ECC, may become vulnerable to the processing power of quantum computers. In this context, it is necessary to rethink the legal category of the digital signature and project regulatory reforms to ensure its validity in a post-quantum environment.

1. Digital signature under Law 527 of 1999

Law 527 establishes that the digital signature is an authentication mechanism based on public-key cryptography, guaranteeing the integrity and authenticity of electronic documents. The principle of technological neutrality allows any reliable method to be considered a digital signature, provided it meets security and functional equivalence standards. This principle must be reinterpreted in light of quantum risks, since legal validity depends on the technical robustness of the algorithms employed.

2. Quantum threat to digital signatures

Advances in quantum computing, particularly Shor’s algorithm, enable the factorization of large numbers and the resolution of discrete logarithm problems in polynomial time, directly undermining RSA and ECC. Likewise, Grover’s algorithm reduces the complexity of brute-force attacks on symmetric systems. These developments imply that current digital signatures may become vulnerable, weakening their evidentiary value in judicial and contractual processes.

3. Verifiable technical elements

The transition to a post-quantum environment requires the adoption of algorithms resistant to quantum attacks. The NIST (National Institute of Standards and Technology) selected between 2022 and 2024 algorithms such as CRYSTALS-Kyber for encryption and CRYSTALS-Dilithium for digital signatures. Similarly, ISO/IEC JTC 1 is working on international standards for post-quantum cryptography applicable to digital signatures. These verifiable technical elements form the basis upon which Colombian legislation must be reformed.

4. Need for reform of Law 527

The reform must explicitly recognize post-quantum algorithms as valid for digital signatures. It should also establish mechanisms for international interoperability with NIST and ISO standards, introduce the principle of technological resilience, and reinforce evidentiary guarantees to ensure that post-quantum digital signatures retain their functional equivalence with handwritten ones.

5. International comparison

In the European Union, the eIDAS 2.0 Regulation discusses the integration of quantum-resistant mechanisms. In the United States, NIST leads the standardization of post-quantum algorithms, directly impacting the validity of digital signatures. In Latin America, Colombia and Mexico have not yet explicitly incorporated the quantum threat into their legal frameworks, creating a regulatory gap and an opportunity for regional leadership.

Conclusions

The digital signature, as a legal category, faces a structural challenge in the quantum era. Reforming Law 527 is essential to recognize the post-quantum digital signature, adopt international standards, and guarantee the continuity of its functional equivalence. The post-quantum future does not eliminate the digital signature but requires its legal and technical transformation. Colombia must anticipate this transition to maintain legal certainty in electronic commerce and strengthen trust in digital transactions.

Gamification of Trading and Consumer Protection in Colombia: The Challenges of Using Foreign Platforms

By Daniel Peña Valenzuela, Partner Peña Mancero Abogados

Introduction

Gamification in trading has become a central strategy for digital platforms to attract and retain users. Through playful elements such as badges, rewards, leaderboards, and visual notifications, trading is transformed into a game-like experience. However, in Colombia, this practice raises serious consumer protection concerns, particularly when foreign platforms operate beyond the direct supervision of the Colombian Financial Superintendence.

This article examines the risks of gamified trading for Colombian consumers, highlights examples of international platforms such as Robinhood, eToro, and Binance, and proposes regulatory and cooperative mechanisms to mitigate digital manipulation in financial markets.

Dynamics of Gamification and Risks for Colombian Consumers

The logic of gamification in trading relies on behavioral stimuli designed to encourage frequent transactions. These stimuli, such as badges or visual rewards, create a sense of immediate achievement that can push users to repeat actions without properly assessing risks. A clear example is Robinhood in the United States, which was criticized for using digital confetti after trades, reinforcing emotional bias toward repeated trading.

Risks for Colombian consumers are significant. Gamification exploits behavioral biases such as loss aversion and the illusion of control, leading to impulsive decisions. Moreover, the extraterritoriality of platforms like eToro, based in Cyprus, or Binance, registered across multiple jurisdictions, makes direct oversight by the Colombian Financial Superintendence difficult. Finally, the information provided by these platforms often fails to meet the transparency standards required under Law 1480 of 2011, leaving consumers exposed.

Practical examples highlight these dynamics. Robinhood encourages high-frequency trading through simple interfaces and attractive visual cues. eToro promotes “copy trading,” where users replicate other investors’ strategies, potentially leading to uninformed decisions. Binance offers rewards and gamified token use, exposing consumers to volatile assets and increasing financial risk.

Conclusions

Gamified trading poses a challenge to consumer protection in Colombia. While it fosters financial inclusion, it also exposes users to manipulation and excessive risk. Needed measures include:

- International cooperation: bilateral and multilateral agreements to supervise foreign platforms.

- Warning protocols: clear digital messages about behavioral and financial risks.

- Financial education: programs teaching consumers to identify gamification techniques and their effects.

- Adaptive regulation: rules integrating consumer protection principles for digital and cross-border platforms.

Alliott Global – Client Alert Colombia | 2026 Long-Term Renewable Energy Auction (Renewables & Storage): cross-border entry routes and near-term opportunities

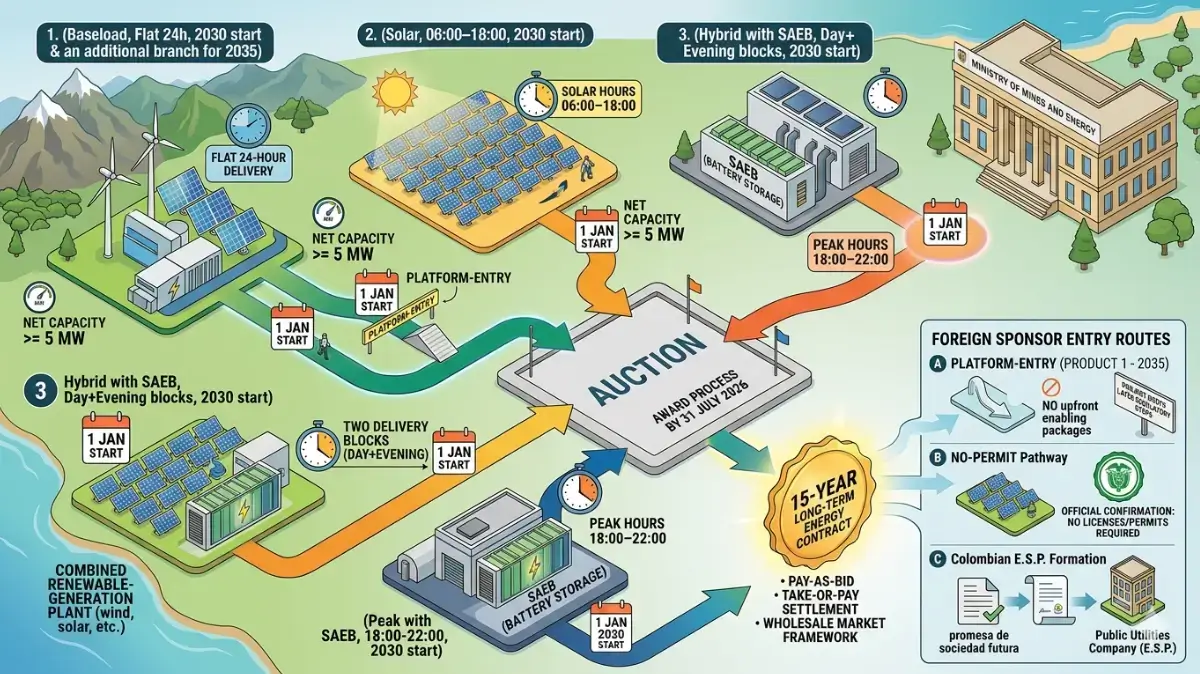

Colombia’s Ministry of Mines and Energy has launched a new long‑term energy contracting mechanism, with the auction award process to be implemented no later than 31 July 2026.

Successful participants will enter into Long‑Term Energy Contracts with a 15‑year term starting from the contract obligations start date, under a pay‑as‑bid allocation design and a “take-or-pay‑contract” settlement approach within the wholesale market framework.

Contract pricing is based on the seller’s bid price plus the applicable regulated component (CERE), as provided in the auction rules

What is being auctioned?

The mechanism offers four (4) products differentiated by hourly delivery profile:

- Product 1 (Baseload): Flat delivery across 24 hours.

- Product 2 (Solar): Delivery aligned to solar hours 06:00–18:00 (12 hours).

- Product 3 (Hybrid): Two delivery blocks (day + evening) and participation requires the plant to include a SAEB (battery energy storage system) among its generation assets.

- Product 4 (Peak): Flat delivery 18:00–22:00 and energy must be delivered through a SAEB integrated as part of the generation assets.

The contracts will generally start on 1 January 2030. For Product 1, an additional auction will be held for contract starting on 1 January 2035.

Foreign sponsors: practical entry without an existing Colombia presence

For sell-side participation, the rules expressly allow foreign individuals and entities to participate through a Colombian participation structure, including a “company formation undertaking” (promesa de sociedad futura) to incorporate a Public Utilities Company (E.S.P.) domiciled in Colombia, which would assume the rights and obligations of a generator if awarded

Fast-track ways to participate (before 31 July 2026)

Two practical entry routes stand out for sponsors seeking a lighter upfront path into Colombia’s long-term contracting auction

- Product 1 with a 2035 start date: a straightforward “platform-entry” option. This track does not require the typical enabling packages at the time of participation, while the project still needs to meet the applicable regulatory steps over the course of development.

- “No-permit” projects: for smaller or lower-impact assets, sponsors may also pursue projects that can be supported with an official communication from the competent environmental authority confirming no environmental licenses, permits, authorizations are required.

Quick eligibility screen (minimum scale)

- Product 1: participation is available for: (i) new plants (renewables) with net effective capacity ≥ 5 MW; (ii) certain existing renewable plants meeting the applicable conditions, and (iii) new self-generators (autogenerators) with surplus ≥ 5 MW.

- Product 2: Reserved for new Solar PV plants and new solar self-generators with surplus, in each case with net effective capacity / surplus ≥ 5 MW

How Peña Mancero Abogados can support Alliott member clients

- Auction-entry structuring for foreign sponsors (E.S.P. or “promesa de sociedad futura”) and governance documentation.

- Fast eligibility screen identifying the simplest route (Product 1–2035 or “no‑permit” environmental pathway projects and the minimum capacity fit (≥ 5 MW where applicable)

- Auction representation as a client counsel and attorney‑in‑fact for filings, platform steps and bid process coordination with the auction operator.

- If awarded, support the auction‑operator mandate agreement for centralized contract/guarantee administration and the required market registrations and ongoing energy market compliance to operate and settle under Colombian rule.

Contact

Gabriela Mancero – Partner | gabrielam@pmabogados.co

Mauricio Torres – Energy & Infrastructure | mauriciot@pmabogados.co

Reimagining arbitration: the 2026 ICC rules revision

By Daniel Peña Valenzuela, Partner Peña Mancero Abogados

Introduction

The 2026 revision of the ICC Arbitration Rules represents a major step forward in how international disputes are resolved. For business leaders and entrepreneurs, these changes are not just technical—they directly affect how quickly, transparently, and cost-effectively disputes can be managed. The reforms emphasize efficiency, digital adaptation, and institutional flexibility, making arbitration more aligned with the realities of global commerce.

1. Procedural Flexibility and Case Management

- Terms of Reference: Previously a mandatory document, now optional. This reduces paperwork and speeds up the start of proceedings. However, any new claims after the first case management conference must be approved by the tribunal, ensuring control and predictability.

- Early Determination: Tribunals can now dismiss clearly unfounded claims early, saving time and resources for businesses.

- Truncated Tribunals: If an arbitrator leaves after the final hearing or submissions, the remaining arbitrators can continue without delay, avoiding costly interruptions.

- Case Management Techniques: While removed from the formal rules, guidance will still be available through ICC reports and notes, offering practical tools for efficient case handling.

2. Transparency and Independence

- Disclosure Standards: Arbitrators must disclose relationships as before, but now parties must also list related entities. This increases clarity and reduces risks of hidden conflicts.

- Confidentiality: Arbitrators are explicitly bound to confidentiality, reassuring businesses that sensitive information will remain protected.

3. Digitalization and Technological Adaptation

- Electronic Communication: Digital communication is now the default, reducing delays and costs associated with physical correspondence.

- Electronic Signatures: Awards can be signed electronically, even in multiple counterparts, with parties choosing between electronic or paper notifications. This modernizes the process and aligns with business practices.

Expedited and Highly Expedited Procedures

- Expedited Procedure Threshold: Raised to USD 4 million, meaning more mid-sized disputes can benefit from faster resolution.

- Highly Expedited Procedure: A new fast-track option with a 3-month timeline, limited steps, and even the possibility of unreasoned awards. This is ideal for businesses seeking quick closure without extensive litigation.

Emergency and Interim Measures

- Ex Parte Measures: Emergency arbitrators can now order urgent measures without hearing the other party first, strengthening protection in critical situations.

Institutional Oversight and Administrative Efficiency

- Fee Decisions: The Secretary General now has more flexibility in deciding fees, potentially making costs more predictable.

- Tribunal Secretaries: Officially recognized as administrative support, but without decision-making powers, ensuring clarity in their role.

Conclusions

For businesses, the 2026 ICC Rules Revision signals a more practical and business-friendly arbitration environment. By embracing digital tools, streamlining procedures, and reinforcing transparency, the ICC has made arbitration faster, clearer, and more adaptable to modern commercial needs. These reforms reflect a shift from arbitration as a purely legal process to arbitration as a strategic tool for safeguarding efficiency, fairness, and trust in global business relationships.

The revised ICC Rules will enter into force on June 1, 2026, applying to all new arbitrations filed from that date onwards. For companies, this means that any disputes arising after the start of the year will already benefit from the modernized framework. Businesses should take note of these timelines to adjust their contractual strategies and dispute resolution clauses, ensuring they are aligned with the new, more efficient and transparent system.

The illusion of exit: Colombia, ICSID, and the politics of investment reform

By Daniel Peña Valenzuela, partner Peña Mancero Abogados

Since the 1990s, Colombia relied on bilateral investment treaties (BITs), ceding partial jurisdictional sovereignty to international arbitration tribunals, especially ICSID.

Withdrawal from ICSID or BITs does not eliminate obligations: survival clauses extend protections for 10–20 years, ensuring ongoing claims and enforceable awards.

Regional precedents (Bolivia, Ecuador, Venezuela) show that denunciation did not prevent litigation or financial liability; states continued to face numerous claims and costly awards.

Academic studies confirm BITs are not decisive in attracting foreign direct investment; structural variables such as economic size, per capita income, and geographic distance matter far more.

Investor-friendly clauses (fair and equitable treatment, umbrella provisions, intellectual property protections) have constrained national sovereignty, limiting policy space in areas like environment, health, and education.

Colombia’s participation in UNCITRAL negotiations since 2017 reflects broader reform efforts, aiming to establish a permanent multilateral investment court with independent judges.

The current debate is more political than practical: withdrawal does not alter the immediate status quo but opens space to reconsider Colombia’s long-term investment policy.

Legal obligations non-profit organizations (ESALES) 2026

CAUSE FOR DISOLUTION OF COMPANIES DUE TO NON-COMPLIANCE WITH THE HYPOTHESIS OF CONTINUING BUSINESS